in this article, we take a look at which current courses are popular options for furthering your education, as well as explain how taking a personal loan with NCL can leave you feeling empowered to take the important leap of forging the future you feel you were meant to have. Added to this, using the RCS Loan Calculator, you can work out what your course is likely to cost monthly.

In an article published by BusinessTech earlier this year, they released the current list of the top 20 in-demand jobs in South Africa. This is often a good starting point for people looking to study, as it indicates areas where the best gaps in the job market are. The list was based on jobs advertised over the course of 2023:

- Middle/Department Management

- Software Development

- Representative/Sales Consulting

- Financial/Project Accounting

- Systems/Network Administration

- Admin Clerk

- Bookkeeping

- Senior Management

- Team Leaders & Supervisors

- Data Analysis/Data Warehousing

- Business Analysis

- Building Project Management

- Accounts Payable/Receivable

- Business Development

- Purchasing & Procurement

- Human Resources

- Executive Management/Director

- Client/Customer Support

- Account Management

- Cost & Management Accounting

The list above indicates opportunities across various industries, and taking a strong business course could assist you in either breaking into one of the sectors, or aid you in being able to apply for a senior or managerial role.

The list above indicates opportunities across various industries, and taking a strong business course could assist you in either breaking into one of the sectors, or aid you in being able to apply for a senior or managerial role.

For example, a Software Engineering Bootcamp through Stellenbosch University will set you back R44 900. Using the NCL personal loan calculator, you can work out that paying the loan for the course back over three years (36 months) will cost around R2,429.62 per month on a R50 000 loan.

If you’ve been climbing the corporate ladder and are looking for a boost to your business management skills, you could look for something like CPUT’s Business Management short course. This 10-week course is geared for owners and managers of small and medium businesses who need to improve their managerial skills, and costs R8000. Using the NCL loan calculator indicates that you can pay for this course with a R10 000 personal loan, and still have some change for any studying-related material you may need. Taking the loan over 12 months will set you back R 1,185.77.

Bookkeeping is a highly-desired skill at present, and heading to Damelin Online will allow you to take a 10-week short course to brush up your number crunching skills. This course costs R11 828.30 and consists of 10 modules. Using the NCL loan calculator, you can work out that a R12 000 loan taken over 24 months would mean that you will only pay around R839.62 per month! Using the Secure loans calculator will help you easily budget for your studies and a personal loan is an ideal product to deal with shorter courses or studies that can enhance your career trajectory while you continue working. Completing these studies, although at a cost, can fast-track your route to promotion and in turn, assist in improving your monthly earnings – offering a long-term impact on your financial situation.

Using the Secure loans calculator will help you easily budget for your studies and a personal loan is an ideal product to deal with shorter courses or studies that can enhance your career trajectory while you continue working. Completing these studies, although at a cost, can fast-track your route to promotion and in turn, assist in improving your monthly earnings – offering a long-term impact on your financial situation.

Whether you want to apply for a loan online, or simply use the loan calculator for budgeting purposes, head to the NCL website now.

How Does Interest Rate Work?

People borrow money for various reasons, like buying a house, starting a business, or leasing a car. Lenders charge interest on these as the cost of borrowing.

People also save their money in banks, which pay interest for allowing them to use the depositor’s money.

Interest rates are calculated by taking into account the principal loan amount and any applicable fees or charges.

The interest rate determines how much money you will have to pay back during the life of your loan.

Higher interest rates are charged when the risk of default is greater.

For instance, if you have poor credit or are applying for a loan with no down payment, the lender may view you as a higher risk and charge a higher interest rate.

Interest rates also vary depending on the type of loan.

For example, mortgages typically have lower interest rates than credit cards since houses are considered reliable investments that will keep their value over time, while credit cards are seen as liabilities.

Similarly, you lend banks money in the form of your deposits.

They pay interest rates as compensation for their use of your money to fund loans, investments, and other activities. The Federal Reserve determines deposit interest rates.

Interest Rate Calculation

Interest rates can be simple or compounded. Simple interest is a fixed rate applied to the principal loan or deposit amount, while compound interest applies an additional rate on any accumulated interest from previous periods.

Compound interest is also known as “interest on interest.”

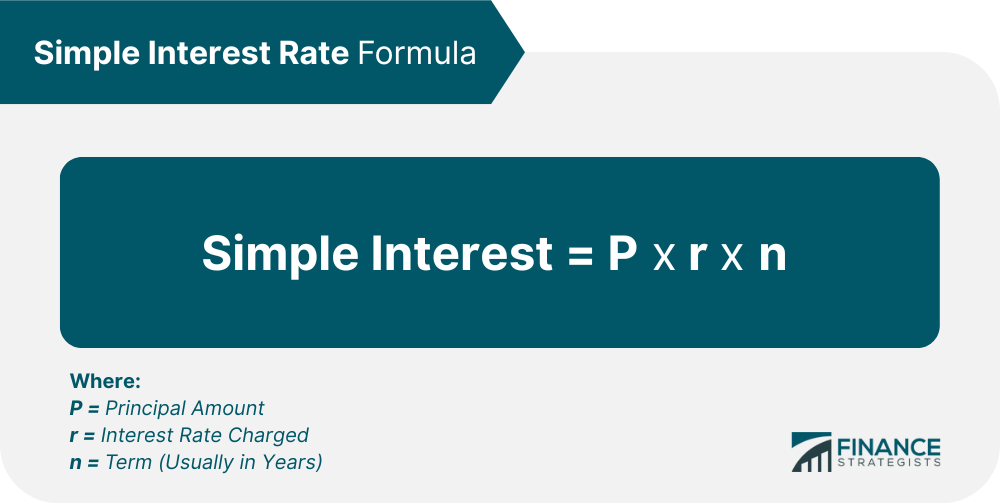

Simple Interest Rate

Simple interest is the principal amount multiplied by the interest rate charged multiplied by the term, such that:

For example, if you borrow $3,000 at a 4% interest rate for 3 years, the total amount of simple interest paid over the life of the loan using the formula above is $360 ($3,000 x 0.04 x 3).

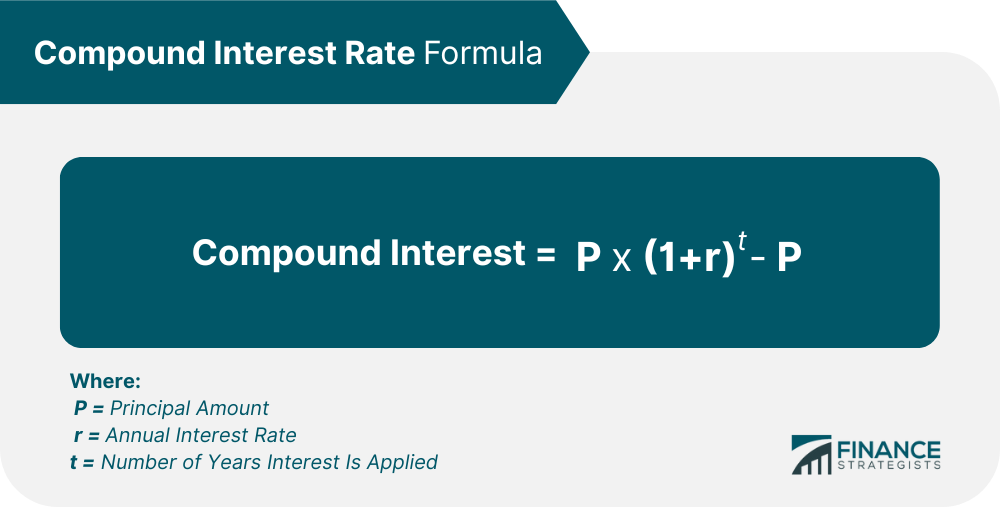

Compound Interest Rate

Compound interest is calculated by multiplying the principal amount by one plus the annual interest rate raised to the number of years interest is applied, minus the principal, to wit:

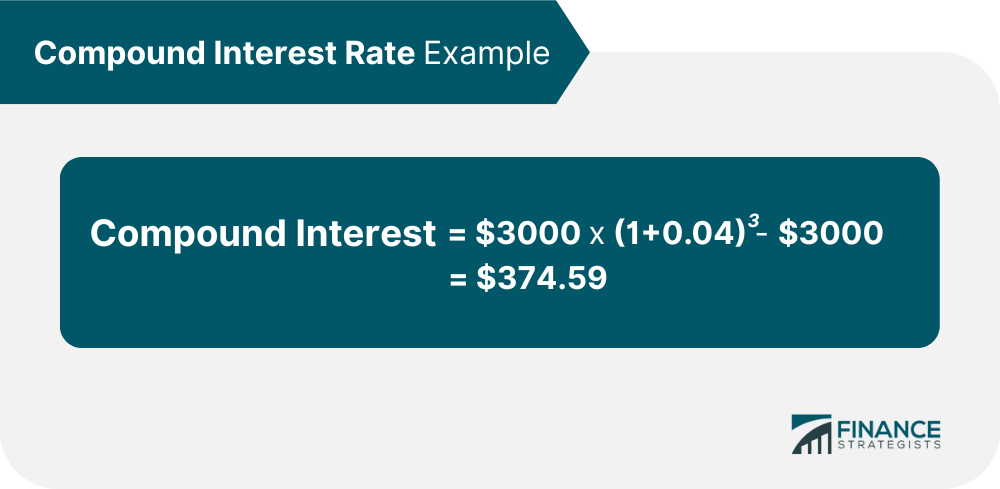

For example, you borrow $3,000 with an interest of 4% compounded annually for 3 years. Using the above formula, the total amount of compound interest paid over the life of the loan is $374.59.

Notice from the examples that compound interest is greater than simple interest even with the same principal amount.

The reason is that compound interest is charged on the principal plus the accumulated interest from previous years of the loan.

Types of Interest Rates

Interest rates can be further classified depending on the effects of key economic factors like inflation. They can be nominal, real, or effective interest rates.

Knowing the difference between the three can help you make better decisions when borrowing or investing and better understand the total cost of a loan or return on a deposit.

Nominal Interest Rate

The nominal rate is the stated annual interest rate charged on a loan or returns on a deposit.

Also known as coupon rate, it does not consider any additional fees or costs associated with the product or the effects of inflation.

For example, a bank’s advertised interest rate is typically nominal, say a 4% annual yield for a six-year certificate of deposit (CD).

Focusing solely on the nominal interest rate can result in overlooking important details and creating false expectations on total charges or returns.

Real Interest Rate

The real interest rate considers inflation by subtracting expected future price increases from the nominal rate.

For example, if a loan or deposit has an 8% nominal interest rate, but 5% inflation is expected for the year, the real interest rate would actually be 3%.

Real rates are more useful for comparing various investment options over long-term periods, as they help you determine the true return on an investment after inflation.

Effective Interest Rate

The effective interest rate is the actual return on deposit or borrowing cost after considering the compounding of interest and all associated fees and charges.

This rate can be calculated from the nominal rate and frequency of compounding.

For example, a six-year $1,000 CD that offers 4% compounding interest annually will yield a total of $265.32 effective interest after the allotted period.

The effective interest rate gives a more accurate picture of the entire loan or deposit product.

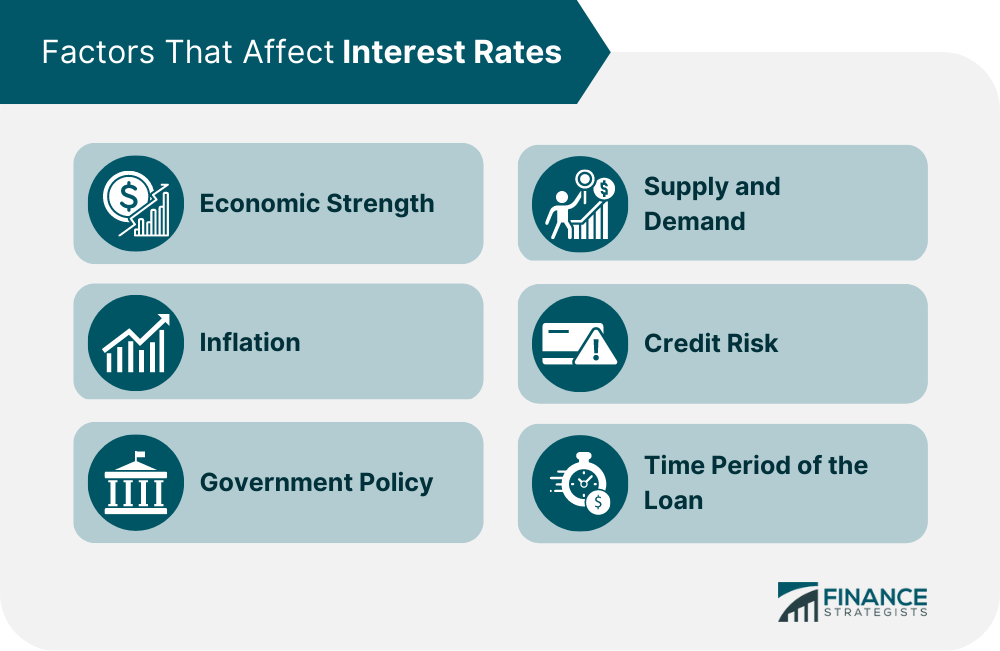

Factors that Affect Interest Rates

While interest rates affect investment returns or loan repayment costs, it is also influenced by factors like the economy’s strength, inflation, supply and demand, government policy, credit risk, and loan period.

Economic Strength

A strong economy with low unemployment increases demand for goods and services, which can increase rates as businesses attempt to borrow more money to meet this demand.

On the other hand, a weak economy results in lower interest rates as lenders are less confident about lending their money due to the increased risk of default and decreased need for borrowing.

Inflation

When inflation rises, so too do interest rates. This is because lenders require a higher rate of return on their investment to make sure they do not lose out on purchasing power due to rising costs of goods and services over time.

In such a scenario, borrowers must pay back more than the principal amount due to the currency’s depreciation.

Government Policy

The government also plays an important role in determining interest rates, as they use these to influence economic policy.

For example, the Federal Reserve can raise or lower short-term interest rates to manage inflation and stimulate the economy.

These changes usually have a ripple effect that affects other interest rates, such as mortgage and credit card rates.

Supply and Demand

Interest rates are ultimately determined by supply and demand. When there is high demand for credit, lenders can increase their rates as they have more opportunities to lend out money at higher returns.

On the other hand, when there is a low demand for borrowing, lenders will lower their rates to make their services attractive to potential borrowers.

Credit Risk

Generally, the riskier a loan is deemed by a lender, the higher the interest rate a borrower must pay.

This makes sense as it incentivizes lenders to take on more risky investments and compensates them for the higher chance of default.

High-risk loans normally come with a base rate and a risk premium. The latter considers the borrower’s credit risk and accordingly affects how much interest they will have to pay.

Time Period of the Loan

The length of the loan can also significantly affect interest rates.

Generally, the longer the loan period is, the higher the rate will be to cover any additional risks incurred by lenders over time.

For example, short-term loans come with many benefits, such that a 3 or 6-month installment loan usually comes with lower rates compared to long-term ones such as mortgage or car finance loans.

Annual Percentage Rate (APR) vs Annual Percentage Yield (APY)

Annual percentage rate and annual percentage yield are commonly used terms when discussing interest rates. They are both expressed as percentages but have different implications.

The APR is the interest you will be charged when you borrow. The APY is the interest you get when you save.

A higher APR is often associated with a loan. It includes not only the interest rate on the principal amount of a loan but also any fees charged by the lender, such as points, origination fees, and other costs involved in obtaining credit.

A higher APR indicates a higher cost of borrowing.

On the other hand, APY calculates how much return you can expect on an investment over a 12-month period and considers both compounding interest and other fees associated with the investment.

When looking for an investment vehicle, it is best to look for one with a higher APY, which means more of your money will be returned to you through compound interest or other benefits.

You may also consult with a financial advisor to assist you with your savings or loan needs. https://www.youtube.com/embed/ovbIVJnF3_E

Final Thoughts

Interest rates indicate the cost of money. They are a key factor to consider when it comes to borrowing or investing.

Further, they give you an idea of how much you need to repay or what investment returns you can expect.

Interest rates can be calculated as either simple or compounded. Further, they can be classified depending on the effects of key economic factors. They can be nominal, real, or effective interest rates.

Factors that affect interest rates are economic strength, inflation, government policy, supply and demand, credit risk, and loan period.

There are two standard terms when discussing interest rates. The APR is the interest you will be charged when you borrow. The APY is the interest you get when you save.

Whether you are a lender, a borrower, or both, it is critical to evaluate how changing interest rates may affect your financial decisions.